10 Oct Understanding the French Wealth Tax (IFI)

What Is the IFI?

The Impôt sur la Fortune Immobilière (IFI) — or French Real Estate Wealth Tax — applies to individuals whose net real estate assets in France exceed €1.3 million as of January 1st of each tax year.

It replaced the former general wealth tax (ISF) in 2018 and now focuses exclusively on real estate holdings, whether owned directly or indirectly.

Who Is Liable?

French tax residents are taxed on their worldwide real estate assets and non-residents are only taxed on real estate located in France. If you own property through a company (such as an SCI or a foreign structure), its underlying real estate value may still be included in the calculation.

What Assets Are Subject to IFI?

The IFI applies only to real estate assets that contribute to your private wealth. This includes properties you own directly—such as your primary residence, secondary homes, rental investments, or land held for development. It also extends to indirect ownership, for example through a French property company (SCI) or any structure whose main purpose is to hold real estate. Even shares in a real estate investment vehicle, like an SCPI or OPCI, are taken into account based on the portion of their value that corresponds to property assets.

On the other hand, assets connected to your professional activity are excluded if they are genuinely used for business purposes. Likewise, financial assets such as bank accounts, listed shares, bonds, or life insurance contracts are outside the IFI’s scope, as are movable goods like cars, art, or furniture.

In essence, the IFI focuses purely on real estate wealth, distinguishing it clearly from broader forms of capital or investment income.

How Is It Calculated?

The IFI is based on your net taxable real estate value, meaning:

Total real estate assets – eligible debts = taxable base

Debts may include:

- Outstanding property loans.

- Renovation or repair expenses due.

- Notary and acquisition fees still owed.

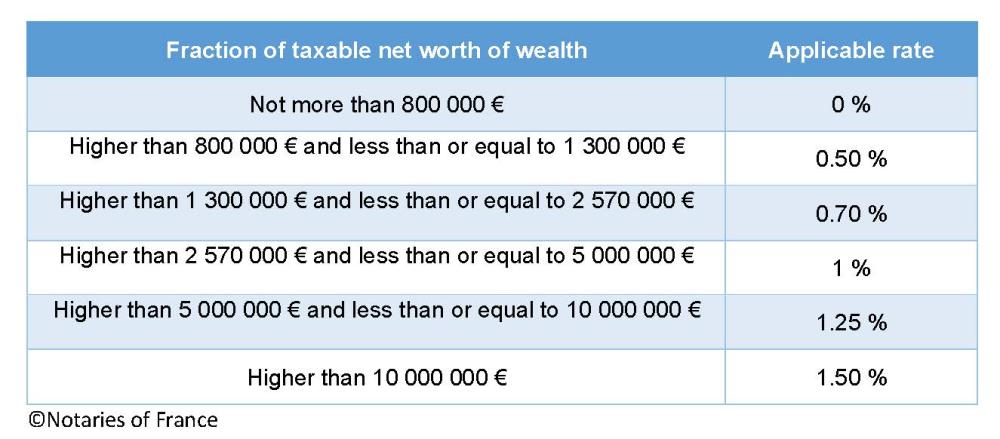

Once the net value is determined, the following progressive tax scale applies:

On the other hand, assets connected to your professional activity are excluded if they are genuinely used for business purposes. Likewise, financial assets such as bank accounts, listed shares, bonds, or life insurance contracts are outside the IFI’s scope, as are movable goods like cars, art, or furniture.

In essence, the IFI focuses purely on real estate wealth, distinguishing it clearly from broader forms of capital or investment income.

Example: How IFI Works in Practice

Let’s imagine a client purchasing a property in France worth €2 million. If the purchase is made entirely in cash, the whole amount counts as taxable real estate wealth. After applying the progressive IFI scale, the total tax would come to approximately €7,400 per year.

However, if the same client finances the purchase with a €1.5 million mortgage, only the net real estate value — that is, €2 million minus €1.5 million in outstanding debt — is considered for IFI purposes. The remaining €500,000 falls below the €800,000 threshold, meaning no IFI would be due.

This simple example shows how financing can play a major role in optimizing one’s wealth tax position. Strategic use of debt not only supports property acquisition but can also help manage or even eliminate exposure to the IFI, as only net property value is taxable.

Declaration and Payment

IFI is declared along with your annual income tax return (Form 2042-IFI).

Payment is due in the summer following the declaration.

Foreign owners without other French income obligations can file a standalone IFI return.

https://www.impots.gouv.fr/formulaire/2042-ifi/declaration-dimpot-sur-la-fortune-immobiliere

Sorry, the comment form is closed at this time.